Leasing a vehicle offers flexibility you don’t find with owning your own vehicle or taking out an auto loan. However, getting into a wreck when leasing a vehicle can be more complicated, with most people not knowing where to turn.

If you’re driving a vehicle you don’t own, knowing what happens next and how to claim compensation is crucial for ensuring you’re not left out of pocket by a negligent driver. For legal guidance, consult an experienced Austin car accident lawyer to protect your rights. Let’s discuss everything you must know about what happens when leased cars are in an accident and – more importantly – who pays.

Key Takeaways

-

Leased vehicles are rented for a set period from the original owner. During your lease, you assume all responsibility for repair, maintenance, and insurance coverage.

-

Your auto insurance provider or the other driver’s auto insurer will pay for the damages to a leased car, depending on who’s at fault, and up to your insurance’s coverage limits minus your deductible.

-

Repairs to a leased vehicle may need to be done at an authorized service center or via the leasing company’s in-house team.

-

If a leased car is totaled, meaning the repair costs are more than 65% of the car’s total value, your insurance will pay the determined value of the car at the time of the crash. If this is less than the leasing company’s value, gap insurance can make up the difference and prevent you from paying out of pocket.

-

You’re obligated to report all leased vehicle accidents to both your auto insurance provider and the leasing company, or you may risk invalidating your coverage and incurring financial penalties on the lease.

-

If you’re involved in an accident in a leased car, contact an experienced personal injury lawyer to ensure your legal rights are protected and win the maximum amount of compensation.

What is a Leased Car?

Leasing a vehicle is a contractual arrangement whereby you buy the right to use someone else’s car for a set period. As part of the lease, you’ll make monthly payments to maintain it. These payments are usually determined as a percentage of the vehicle’s total value before the lease is signed.

When you lease a vehicle, you assume responsibility for maintenance, repairs, and auto insurance. That’s important because it influences what happens if you’re involved in a car accident while driving a leased vehicle.

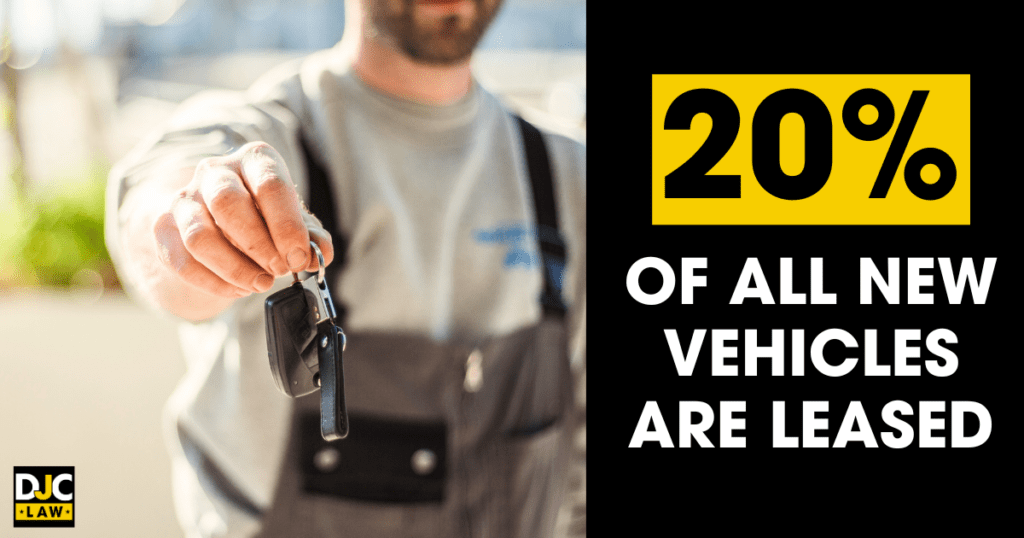

According to Forbes, around 20% of all new vehicles are leased. However, unlike taking out an auto loan, you won’t own the vehicle at the end of the contract. Typically, most leases last around three years. After your lease elapses, you must either return the vehicle to the owner or renew the lease.

In some cases, you might even be able to purchase the vehicle, but none of the lease payments you made will count toward it if you decide to go with this option.

What’s the Difference Between a Leased Vehicle and a Rental Car?

The only difference between a car lease and a car rental agreement is the length. Renting a car means you’re likely only going to drive the car for a few days or weeks. In contrast, leases are measured in years. The typical lease is three years, but some companies may offer shorter or longer leases.

How Does an Accident Affect a Car Lease?

Crashing a leased car is much the same as crashing your own car. You’re still required to pay the costs of repairing the vehicle through your auto insurance provider. On the other hand, if you total the car, your lease will usually be terminated.

It’s vital to check your leasing agreement because you’ll typically have a time frame to report an accident. If you fail to report it, your lease could be terminated, and there may even be financial penalties attached.

Generally, you won’t necessarily see your lease terminated just because you got into a minor fender-bender. In 2022, the National Highway Traffic Safety Administration (NHTSA) reported that 2.38 million Americans were injured in car accidents. If you’re one of these accident victims, your own insurance may even provide a rental car while your leased car is repaired.

Note that as part of your lease, you may be required to go about repairs in a specific way. Typically, you can’t start using parts from different manufacturers, which is why calling your leasing company and asking for guidance is critical. Plus, some car lease companies may only allow you to use a short list of garages in your area.

What to Do After a Leased Car Accident

After a leased car accident, you must follow the proper steps to protect your health and avoid violating the terms of your lease. These steps include calling 911, exchanging insurance details, documenting the scene, and notifying your insurer and leasing company.

According to the Insurance Information Institute (III), your chances of being involved in an accident are 1 in 366 per 1,000 miles, so it’s not as rare as you think. Generally, you want to follow these steps after a leased car accident:

-

Call 911 – The first step is calling 911 to get any injured parties the medical attention they need. If nobody is injured, state law may still require you to notify law enforcement and wait until an officer attends to fill out a police report. For example, the Texas Department of Transportation reveals that accidents must be reported if there’s an injury, fatality, a vehicle can’t be moved, or property damage exceeds $1,000.

-

Exchange Information – You must exchange information with any other drivers. Typically, this will be your contact and insurance details, alongside license plate numbers. Driving away without exchanging details is a crime and could land you in jail.

-

Document the Scene – Use your smartphone to take photos and videos of the scene. Focus on visible injuries, vehicular damage, and property damage. It’s also the time to take down the details of any eyewitnesses who may be willing to provide statements later.

-

Seek Medical Attention – Seek medical attention immediately after leaving the accident scene. You might feel okay, but that doesn’t mean you don’t have hidden injuries. Conditions like whiplash and concussion may take a few hours to a few days to start showing visible symptoms.

-

Tell Your Insurance Company – Report your accident to your insurance company. Most auto insurers require all accidents to be reported within 24-72 hours of the accident.

-

Tell Your Leasing Company – You’ll also be expected to report the incident to your leasing company. They’ll tell you what your next steps are and explain what this means for your lease.

Dealing with medical providers, auto insurers, and leasing companies is always a headache when processing the trauma of an auto accident. Contact an attorney and seek legal counsel. They’ll explain your legal rights, navigate complex legal paperwork, and ensure your rights are protected at every turn.

How Do I Get My Leased Vehicle Repaired?

Leased vehicle repairs must be handled with care. Typically, your auto insurance coverage will cover repair costs and any other damage, as it would if you owned the vehicle. If you have additional coverage, your insurer may also cover rental car costs if your leased vehicle is out of action for an extended period.

Don’t immediately take your car to the nearest garage for repairs. Every car leasing company has its own repair policies, including the parts that may be used and options for where to take it. In some cases, the leasing company may even have an in-house team they use exclusively for repairs.

What if a Leased Car Driver Caused the Accident?

Getting into an accident with another leased car doesn’t change what happens next, only who pays. With the cost of car accidents hitting $470 billion in 2022, per the U.S. Centers for Disease Control (CDC), this is likelier than you think. If a leased car driver is at fault, their insurance will cover the costs.

Taking Out Gap Insurance

Gap insurance is an optional but essential add-on for leased vehicle drivers. If your vehicle is totaled, your insurance company may not cover the full cost of the vehicle. Gap insurance pays out for the difference between the amount paid off on the lease and the value of the car.

It’s an optional extra, but it’s one that all car leasers should explore, as it can save you considerable funds out of pocket if a negligent driver totals your vehicle.

Where Should I Take My Leased Vehicle for Repairs?

Where you take your vehicle after an accident depends on the policies of your leasing company. That’s why you must contact your leasing company at the earliest opportunity. The leasing company will tell you what to do and where to take it.

Depending on your lease terms, you may even have several advantages if you paid for add-ons, including:

-

Free rental car.

-

The leasing company covers repair costs.

-

Gap insurance

Note that if you don’t follow the lease’s terms to the letter regarding repairs, you may be required to pay extra charges and fines out of your own pocket. It could also result in the premature termination of your lease.

Who is Responsible for Damages in a Leased Car Accident?

Responsibility for damages in a leased car accident lies with you. Under the terms of standard lease agreements, you assume responsibility for all repairs as if the vehicle were your own. However, leasing companies also require you to show proof of auto insurance, so you’ll either be claiming costs through them or via the other driver’s insurer, depending on who was at fault and whether you live in an at-fault state.

Car repair costs have never been higher. According to a New York Times report, the average cost of a repairable claim has reached $4,700, an 8% year-on-year increase. Nobody wants to pay this out-of-pocket, which is why full coverage auto insurance is critical.

Note that your leasing company may have restrictions in place regarding repairs. For example, you may be required to use an approved car dealership or only use Original Equipment Manufacturer (OEM) parts.

Take the time to read through your lease for a better understanding of your rights and responsibilities.

Does the Leaseholder or Leasing Company Pay for Damages?

The leaseholder is responsible for the damages after a car accident. Lease agreements mandate that you carry and maintain a minimum amount of insurance. Your insurer will pay for the repairs if you’re involved in an accident that wasn’t your fault.

In this respect, the costs of paying the damages on a leased car don’t differ from if you owned the vehicle. If the other driver was at fault, their liability insurance will cover the costs of repairing the leased vehicle.

Note that a deductible is a standard part of an insurance policy. You’ll be required to pay the deductible out-of-pocket before your insurance coverage kicks in. You’re also required to pay for general wear and tear. According to the AAA, car maintenance costs average $800 annually, so you’ll also need to budget for these costs.

How Does Liability Work in a Leased Car Accident?

The concept of liability doesn’t change if you lease a vehicle and you’re involved in an accident. The at-fault driver must pay for all damages and losses unless you live in a no-fault state.

In an at-fault state, the at-fault driver’s insurance company pays for all damages. In a no-fault state, you’ll claim through your own insurance company for damages, regardless of who’s at fault.

Like any car accident, the concept of negligence comes into play. You’ll be required to demonstrate that the other driver was to blame for the accident. In a car accident claim, four thresholds must be met to claim damages:

-

Duty of Care – All drivers have a duty to drive in a way that protects others and complies with the law. In other words, any driver on a public road already has a duty of care.

-

Breach of Duty – You must show that the other driver breached their duty of care. For example, if they were speeding or driving while intoxicated, this shows that they weren’t complying with traffic laws.

-

Causation – The third element of negligence shows that the at-fault driver’s actions or inactions resulted in an accident and losses, such as medical bills, lost wages, car repair bills, and pain and suffering.

-

Damages – Finally, you must demonstrate that any losses suffered resulted directly from the accident. You can’t make a car accident claim if you didn’t sustain any damages.

The system of negligence doesn’t change just because you’re leasing your vehicle. Likewise, you may choose to win compensation via negotiations with the at-fault driver’s insurer or by filing a personal injury lawsuit via an experienced car accident attorney.

The Comparative Negligence Model – Shared Liability

Many states use a comparative negligence model when determining liability. Comparative negligence means blame may be shared if it’s found both drivers contributed to the accident.

Each state sets its own rules regarding shared liability, but the general rule is that any compensation award will be reduced based on your contribution to the accident. For example, if you’re found to be 20% at fault and receive $100,000, your final award will be $80,000.

Check your state’s laws on comparative negligence. For example, Texas has a 51% bar rule that stipulates if you’re 51% or more to blame for an accident, you’re barred from receiving financial compensation for your losses.

What if Another Driver Was At Fault?

If another driver was at fault for an accident, their insurance company will cover the damages via liability insurance. Note that if you live in a no-fault state, your insurance company will pay out for any damages and losses regardless of who was at fault.

Can Lease Insurance Fully Cover the Damages?

Your lease insurance can fully cover any damages. How much they cover and how much it costs you depends entirely on the extent of your insurance policy. As a rule, most leasing companies require you to hold collision coverage and comprehensive coverage.

Note that you may be required to pay a deductible on your auto insurance. As a rule, the higher your deductible, the lower your premiums, but the more you’ll be expected to pay if your car is damaged.

If you’re found to be at fault for an accident involving a leased car, the liability insurance portion of your policy will pay the full repair amount.

How Much Damage is Acceptable on a Lease?

Car lease companies expect a certain amount of wear and tear during the duration of a lease. Minor damage may not incur additional charges, such as minor scratches, dents, and minimal windshield chips. However, significant damage, including catalytic converter damage and damage to the underside, may invite penalties and charges.

Examples of damage that would invite penalty charges include:

-

Large scratches and dents

-

Tire damage

-

Electrical damage

-

Broken windows

-

Missing parts

Any penalties will be outlined in your lease agreement. If you’re charged penalties for excessive damage, the lease company will assess and value the damages before sending you the bill. Any damage believed to have resulted from an accident (no matter how minor) may also command charges because you’re expected to report all accidents to your leasing company.

What Happens if You Total Your Leased Car?

Totaling your vehicle means the repair costs exceed 65% of the car’s total value. Your insurance company will make this judgment based on their valuations. In this case, your insurer will pay the value of the car up to your coverage limits minus your deductible. This could be less than the value of the car to the lessor.

Let’s say that your vehicle is totaled and your insurance company is only offering $5,000, but the car is deemed to be worth $7,000 by the leasing company. That means you owe the lessor $2,000 to cover the difference.

That’s why gap insurance is a wise decision. The purpose of gap insurance is to cover this $2,000 difference so that you’re not left paying a substantial sum out of your own pocket if your vehicle is totaled.

Of course, if you weren’t at fault for the accident, you can file a claim against the at-fault driver’s insurance to recoup any costs.

Can You Return a Leased Car After an Accident?

Drivers may return a leased vehicle after an accident, but it’s usually not the most cost-effective option. The leasing company will charge you for repairs if you go through them. Instead, it’s usually better to repair the vehicle yourself and then make a claim through your auto insurance provider.

How much you’re charged to return a car after an accident depends on the extent of the damage. Extremely minor damage might not incur any extra charges at all. If you total the vehicle, you’ll have to pay off the remaining lease, which could cost you thousands of dollars.

How Does Car Insurance Work on a Leased Car?

Car insurance works the same way on a leased car as on a car you own. Leasing companies usually require a higher amount of coverage when compared to state-mandated minimums. Expect to hold comprehensive and collision coverage at a minimum.

It’s also standard practice for lessors to require higher insurance limits on bodily injury. For example, it’s not uncommon for lessors to require $100,000 in bodily injury coverage per person and $300,000 per accident.

Here’s what the two most common types of coverage mean:

-

Collision Coverage – Collision coverage pays for damages caused in an accident with a vehicle or stationary object. The coverage kicks in even if you were at fault.

-

Comprehensive Coverage – Comprehensive insurance pays for any damages considered to be outside of your control, such as weather, theft, vandalism, animal accidents, and fire.

Note that coverage requirements for car leases vary by state. Some states may require you to carry medical payments coverage, uninsured motorist coverage, and personal injury protection.

Is Leased Car Insurance More Expensive?

Higher minimum coverage limits for leased cars make car insurance more expensive for these drivers. On the other hand, this is often the trade-off for leasing a car instead of paying high auto insurance loan repayments, so it balances out.

What are the Legal Steps to Settle a Leased Car Accident Claim?

Settling a car accident claim involving a leased car involves working with your insurer, leasing company, and an experienced car accident lawyer to protect your legal rights.

The steps involved in settling these claims include:

-

Reporting – You must report your accident to your insurance company and the leasing company as soon as possible. Typically, you’ll be required to report an accident within 24-72 hours.

-

Legal Representation – Enlist an experienced personal injury attorney to support you in dealing with insurance adjusters and your leasing company to protect your legal rights.

-

Assessment – Your insurance company will evaluate the damages and who was at fault via their insurance adjusters. Remember, the at-fault driver’s insurer will do everything they can to shift the blame to you. That’s where the value of hiring an attorney comes in.

-

Claim – Your lawyer will file a claim against the at-fault driver via their insurance company, detailing your losses and damages. This will usually result in several rounds of negotiations.

-

Payout – Once a figure has been agreed upon, your lawyer will advise you whether to accept or reject the offer. If the offer is satisfactory, you’ll sign and receive your compensation.

Note that if there are issues with disputed liability or the compensation amount, there’s a small chance that your case could go to trial. According to the U.S. Bureau of Justice Statistics, only around 5% of personal injury claims go to court.

How Do You File an Insurance Claim for a Leased Vehicle?

Filing an insurance claim for a leased vehicle is simple enough. Each insurer will have a separate process for filing a formal claim. It may include sending a formal letter, calling them, or going through an online portal. There’s no standardized claim protocol, so you’ll need to consult your insurer for how to do this.

Can Leasing Companies Sue for Damages?

Leasing companies may sue for damages to their vehicles, but it’s extraordinarily rare. Under the terms of a car lease agreement, it’s your responsibility to cover damages and maintain the vehicle. Getting into an accident isn’t grounds for getting sued by the leasing company.

Instead, claims made against drivers who’re leasing a vehicle usually result from breaking the lease terms or refusing to pay for damages. For example, if you fail to keep up with your lease repayments or modify the vehicle, you could be sued if you refuse to pay the penalty fees.

In terms of an accident, you might be sued if you allow your insurance to lapse or your insurance company invalidates your coverage. In both cases, all costs will come out of your own pocket. If you refuse to pay, the leasing company may decide to sue you to recoup their losses.

What Legal Responsibilities Does the Leaseholder Have?

The leaseholder is legally responsible for making regular lease repayments, maintaining a minimum amount of auto insurance coverage, and reporting any accidents to the leasing company.

In short, the leaseholder only gains the right to use the vehicle at the behest of the owner, but they must cover all associated costs, including minor maintenance and repairs. Restrictions will also be in place, including:

-

No modifications

-

Pay any traffic citations

-

Early termination fees

-

Mileage limits

-

Return the vehicle on time

Breaking any of the terms of your lease can incur financial penalties, as outlined in your lease agreement. If you fail to pay, you could be sued for any outstanding amounts and have your lease terminated early.

It underpins the necessity of carefully reading through your lease agreement before signing up to lease any vehicle.

Leased Car Accidents FAQs

Do I need to tell my lease company about a car accident?

Yes, your lease agreement will require you to tell the company if you’re involved in an accident, regardless of how minor. If you’re involved in a minor accident, don’t get tempted to avoid telling them, as this could invalidate your lease and incur financial penalties.

Will an auto insurance company cover a leased car accident?

Your auto insurance provider will cover accidents if you’re leasing a car. Leasing companies require you to hold and maintain auto insurance as a condition of your lease. If your vehicle is totaled, gap insurance coverage can cover the lease balance.

Will an accident increase my lease payments?

Your lease payments stay the same regardless of whether you’re involved in an accident. Beware that if your vehicle has damage that surpasses your insurance limits or you total the car and don’t have gap insurance, you could be forced to cover the difference out of your own pocket.

Note that even if your lease payments won’t be affected by an accident, your auto insurance provider may raise your future premiums.